Companies (Compromises, Arrangements & Amalgamation) Second Amendment Rules 2020: Key Highlights

Shivani Jain | Updated: Jan 06, 2021 | Category: News

In exercise of the powers bestowed by sub sections (1) and (2) of section 469 of the Companies Act 2013 read with section 230 of the same act, the Central Government hereby implement the following rules, to amend and improvise the Companies (Compromises, Arrangements & Amalgamations) Rules 2016, namely, the Companies (Compromises, Arrangements & Amalgamations) Second Amendment Rules 2020.

Further, the said rules are in force from 17.12.2020, i.e., the date of the publication in the Official Gazette.

In this blog, we will discuss the key highlights of the Companies (Compromises, Arrangements & Amalgamation) Second Amendment Rules 2020.

Table of Contents

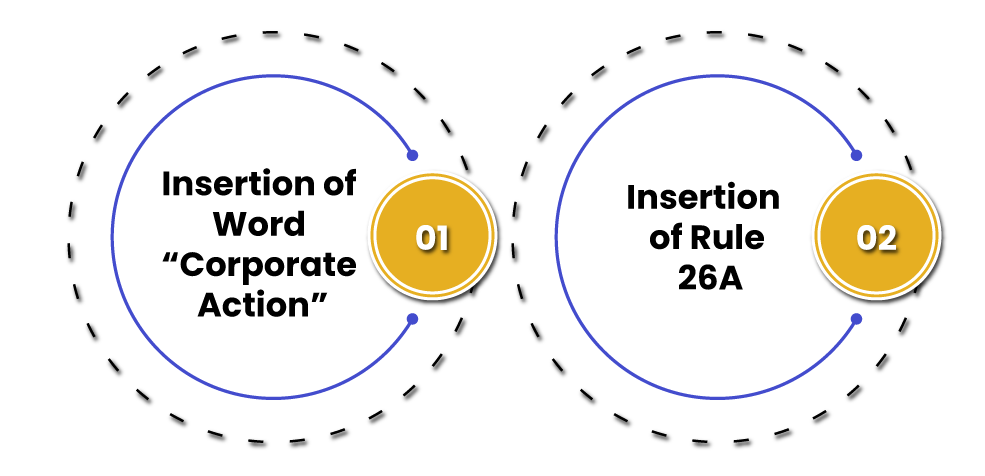

Key Highlights of Companies (Compromises, Arrangements & Amalgamations) Second Amendment Rules 2020

The key highlights of the Companies (Compromises, Arrangements & Amalgamations) Second Amendment Rules 2020 are as follows:

Insertion of Word “Corporate Action”

The Central Government has decided to insert the word “Corporate Action” after clause (d), sub rule (1) in Rule (2) in the said rules.

Further, the term “Corporate Action” denotes any action taken by the company pertaining to the transfer of shares and all the benefits and privileges arising on such shares, specifically, bonus shares, consolidation, split, fraction shares, and right issue to the acquirer.

Insertion of Rule 26A

The MCA or the Ministry of Corporate Affairs seeks to insert Rule 26A in the Companies Second Amendment Rules 2020. Further, this rule relates to the purchase of minority shareholding held in the form of a Demat.

Verification of the Details of Minority Shareholders

According to the new Rule 26 A, a company shall within a period of two weeks, starting from the date of receipt of the amount equal to the share price acquired by the acquirer, under section 236 of the Companies Act 2013, verify the details and particulars of the minority shareholders holding shares in dematerialized form.

Send the Notice to Minority Shareholders

Further, after the process of verification, the said company will send a notice to the minority shareholders regarding the cutoff date, which should not be earlier than 1 month from the date of sending the notice. Furthermore, the term cutoff denotes a date on which the shares held by minority shareholders will be debited from their account and credited to the designated or decided Demat Account of the company. However, it shall be relevant to state that for crediting the shares in the Demat account, the shares need to be first credited in the account of the acquirer, as prescribed in the notice, prior to cut off date.

Publish the Notice in Newspapers

Moreover, the company needs to publish the notice sent to the shareholders in 2 widely circulated newspapers, out of which one will be in English and the other one in the Vernacular Language of the district where the company has its registered office. Also, the same will be uploaded on the official website of the company.

Inform Depository Regarding Cutoff Dates

Thereafter the company will immediately inform the depository regarding the cut-off date and shall submit the declarations stating the following:

- The Corporate Action has been effected in accordance with the provisions of section 236 of the Companies Act;

- All the Minority Shareholders whose shares are maintained in dematerialized form have been duly informed about the Corporate Action;

- The Minority Shareholders will be paid by the company instantly after the successful completion of the Corporate Action;

- Any future dispute or complaints rising out of such corporate action will be the sole responsibility of the said company;

Authorise Company Secretary

For the purpose of carrying out the transfer of shares by way of corporate action, the Board of Directors shall authorize the CS or Company Secretary, or in his/her absence any other person, to notify or inform the depository and submit documents.

Transfer of Shares

Upon receipt of information, the depository will make the transfer of shares into the designated Demat Account of the company. Further, such shares will be transferred on the cutoff date.

Disbursal of Share Price

After receiving the intimation of the successful transfer of shares, the company will now disburse the price of shares transferred on an immediate basis to each of the minority shareholders. Further, the same will be done after deducting the prevailing stamp duty.

Also, such a stamp duty will be paid by the company on behalf of the minority shareholders, based on the provisions of the Indian Stamp Act 1899[1].

Transfer Shares to Acquirer’s Demat Account

Now, after the successful disbursal of share price, the company will inform the depository about the same so that the depository is able to credit the shares kept in the Demat account to the acquirer’s Demat account.

Exception to Transfer of Shares to Acquirer’s Demat Account

In the case, where a court or tribunal, through its order, has restricted the transfer of shares or payment of dividend, then, in that case, the depository will not transfer the shares to the designated Demat Account. Further, the same will prevail in the case where such shares are pledged or hypothecated based on the provisions of the Depositories Act 1996.

Conclusion

In a nutshell, the Companies Second Amendment Rules 2020 majorly deals with two amendments, i.e., Insertion of the word “Corporate Action” and Insertion of section 26A, former deals with the action taken by the company pertaining to the transfer of shares and all the benefits and privileges arising on such shares, whereas, the latter deals with the purchase of minority shareholding held in the form of Demat.

Lastly, in case of any other doubt and dilemma, visit Swarit Advisors, our professionals are always there to cater to your needs and requirements concerning Merger and Amalgamation Companies Second Amendment Rules 2020.

Also, Read: Companies (Appointment & Qualification of Directors) Fifth Amendment Rules 2020: A Detailed Summary