What are the Different Types of Share Capital: A Detailed Guide

Shivani Jain | Updated: Dec 10, 2020 | Category: SEBI Advisory

Every company, whether Private limited or Public limited, needs to have a share capital. Further, the term “Share Capital” denotes the amount contributed by the members of the company to carry out its operations. Also, it shall be relevant to note that a company can alter, modify, increase, or reduce its share capital, subject to certain conditions. Further, there are different types of share capital in a company, and each one provides its own set of rights.

In this blog, we will discuss the concept and different types of share capital available under the provisions of the Companies Act 2013.

Table of Contents

Concept of Share

Section 2 (84) of the Companies Act 2013 defines the term “Share”. According to this section, Share means a part of the share capital of a company that includes stock as well. That means the share is just the part of securities.

Concept of Share Capital

A company being an artificial person has the separate legal existence of its own. That means it needs funds to carry out its working and operations. The term “Share Capital” means the amount contributed by the members of the company in the form of issuance of shares.

Further, it shall be relevant to state that whenever people voluntarily contribute funds in a company, they automatically become the owners or the members of the company. Keeping this thing into consideration, the amount raised by the company is known as Share Capital, and the people contributing are known as Shareholders.

Also, it shall be taken into consideration that, in the case of companies, both “Share Capital” and “Capital” are synonymous to each other.

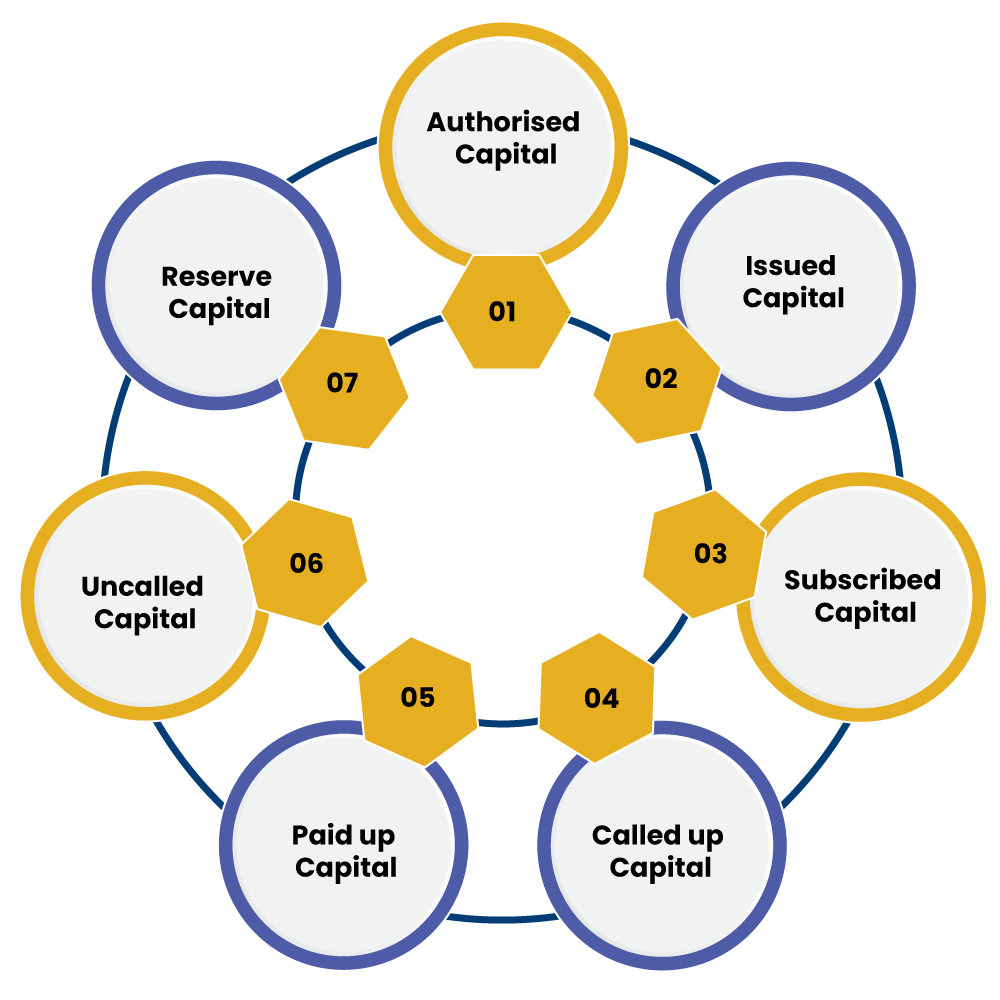

Different Types of Share Capital

As per the provisions of the Companies Act 2013, the different types of share capital are as follows:

Authorised Capital

The term “Authorised Share Capital” means the amount of capital written in the MOA or Memorandum of Association of the company. Thus, it is the amount authorised to be raised by the issuance of shares. Besides this, a company needs to pay the stamp duty on this amount as well.

Further, the other names for Authorised Capital are Nominal Capital and Registered Capital. Also, section 2 (8) of the Companies Act 2013[1] defines the term “Nominal Capital”, as the amount of capital mentioned in company’s MOA.

Moreover, one can calculate the Authorised Capital by taking into consideration the Reserve Capital and Working Capital needs of the company.

Formula For Calculating Authorised Capital

Authorised Capital = Issued Share Capital + Unissued Share Capital.

Issued Capital

The term “Issued Capital” means a portion of the Authorised Capital that is offered by the company to the general public for subscription. It includes the process of Allotment of Shares. Further, section 2 (50) of the Companies Act 2013 defines the term “Issued Capital”.

Also, it shall be considerate to note that it is mandatory for every company to disclose the amount of Issued Capital in its Balance Sheet, in accordance with the Schedule III of the Act.

Formula For Calculating Issued Capital

Issued Capital = Subscribed Capital + Unsubscribed Capital.

Subscribed Capital

The term “Subscribed Capital” is defined under section 2 (86) of the Companies Act 2013, as the amount of capital that has been successfully subscribed by the members of the company. That means it is the total number of shares that the general public takes.

However, if in case a company has mentioned its Authorised Capital by any mode of communication, such as Advertisement, Notice, Official Letter, or Business Letter, etc., then in that case, it must mention its paid up and subscribed capital in equal conspicuous characters.

Called up Capital

As per section 2 (15) of the Companies Act 2013, the term “Called up Capital” means the part of the capital that the company calls for payment. That means it is the total amount that a company calls-up on the shares issued.

Paid-up Capital

The term “Paid-up Capital” means the portion of capital that is actually credited or paid by the shareholders on the shares issued. That means it’s the amount of capital that the company receives back from its shareholders in exchange for the stock or shares issued.

Formula For Calculating Paid-up Capital

Paid up Capital = Called up Capital – Calls in Arrear

Uncalled Capital

The term “Uncalled Capital” is just opposite to the “Called up Capital”. It means the portion of share capital that has remained unpaid by the shareholders.

Reserve Capital

The term “Reserve Capital” means the uncalled capital that is although owned by the company but can be used only at the time of dissolution of the business.

Example of Different Types of Share Capital

Question

Suppose ABC Pvt Ltd. is registered with an Authorised Capital of Rs 1, 00, 00,000, which is further divided into shares of Rs. 10 each. The company has issued 8, 00,000 shares to raise a share capital of Rs 80, 00,000. However, the investors have subscribed only for 6, 00,000 shares. Further, the company has asked for Rs. 4 per share out of Rs.10 (Nominal value of shares), but has received payment for only 5, 50,000 shares.

Solution

Authorized Share Capital (10, 00,000 shares of Rs 10 each) = Rs 1, 00, 00,000

Issued Share Capital (8, 00,000 shares of Rs 10 each) = Rs 80, 00,000

Subscribed Share Capital (6, 00,000 shares of Rs 10 each) = Rs 60, 00,000

Called up Share Capital (6, 00,000 × 4) = Rs 24, 00,000

Paid up Share Capital (5, 50,000 × 4) = Rs 22, 00,000

Call in Arrears (50,000 × 4) = Rs2, 00,000

Conclusion

In a nutshell, every business entity requires funds to carry out its business operations. It can raise the same either internally or externally. Further, Share Capital means the amount contributed by the members of the company in the form of issuance of shares. In total, there are 7 different types of share capital available under the provisions of the Companies Act 2013.

Lastly, in case of any other doubt or perplexity, contact Swarit Advisors, out proficient experts will guide you with the process of registration.