External Commercial Borrowings Under New Framework – An Overview

Karan Singh | Updated: Aug 19, 2021 | Category: RBI Advisory

External Commercial Borrowings (ECB) means borrowing by an eligible resident company from outside India as per the framework designed by the RBI (Reserve Bank of India) in discussion with the Indian Government. The term has been defined in Section 2 (iv) of FEMA (Borrowing & Lending) Regulations, 2018. India, a developing nation, has encouraged the inward flow of foreign capital or money for many reasons. The most famous methods to bring foreign capital are Foreign Portfolio Investment (FPI), Foreign Direct Investment (FDI), and ECB. In this blog, we will discuss about External Commercial Borrowings (ECB).

Table of Contents

What are the Types of External Commercial Borrowings?

ECBS can be categorised into foreign currency designated ECB and rupee (INR) denominated ECB.

- INR Denominated ECB: In this type, ECB is raised in INR (Indian Rupee), and it comprises trade credits beyond 3 years, bonds/floating/debentures/fixed-rate notes (other than completely and forcibly convertible instruments), loans comprising financial lease, bank loans, & plain vanilla Rupee denominated bonds issued overseas.

- FCY Denominated ECB: In this type, External Commercial Borrowings are raised in any convertible foreign currency. It includes FCCBs (Foreign Currency Convertible Bonds), FCEB (Foreign Currency Exchangeable Bond), loans comprising trade credits, bank loans beyond 3 years, bonds/floating/debentures/fixed-rate notes (other than entirely & forcibly convertible instruments), and financial lease.

What are the Benefits of External Commercial Borrowings?

- Lower Interest Rates: As an outcome of a diverse investor base, companies tend to avail loans at minimum interest rates, which they wouldn’t have got within the local limits.

- Enhance Economy: The Government can manage the funds’ flow more towards a particular sector of the economy which will enhance the economy.

- Diverse Investor Base: The worldwide arena aids the companies to get access to diverse investors as per their requirements.

- Fulfilling Larger Necessities: Since the possibility of borrowing is increased by crossing local limits, it aids the companies to fulfil their requirements which might not be achievable within local limits.

- Debt–oriented funds: External Commercial Borrowings not necessarily be equity-oriented; that is it will not dilute the proprietorship of the present members. This will not give voting powers to the lender & retain the control of the present stakeholders of the company.

Role of FEMA Regulations

FEMA, 1999; Foreign Exchange Management (Borrowing & Lending) Regulations, 2018, and Master Directions on ECBs, Trade Credit & Structured Obligations issued by the RBI provide for the ECBs regulation. The Reserve Bank of India has a right to issue Master Directions as per Section 10(4) & Section 11 (1) of the EMA Act, 1999.

Objective of the FEMA Regulations

- To rationalise the present framework of External Commercial Borrowings;

- To develop or improve the ease of doing business in India;

- To regulate lending & borrowing transactions between a party staying in India and a party living outside India;

- To strengthen the Anti-Money Laundering or Combating the Financing of Terrorism framework.

Prohibition on the Drawing of External Commercial Borrowings

Master Directions by the Reserve Bank of India delivers for restricted end-uses, i.e., a negative list that prohibits the utilisation of ECB for definite purposes as enlisted below:

- Equity Investment;

- Real Estate Activities;

- Investment in the Capital Market;

- Repayment of Rupee loans, except in the case of ECB raised for repayment of Rupee loans availed domestically for capital expenses and purposes other than capital expenditure;

- Working capital purposes, except in the case of ECB increased from foreign equity holders, are used for working capital purposes, general corporate purposes, or repayment of Rupee loans & ECB increased for working capital or general corporate purposes;

- General corporate purposes, except in the case of ECB increased from foreign equity holders, are used for working capital purposes, repayment of Rupee loans, or general corporate purposes, and ECB evaluated for working capital or general corporate purposes;

- On-lending to companies for the above activities, except in the case of ECB increased for NBFCs (Non-Banking Financial Companies) for general corporate or working capital purposes, for repayment of Rupee loans availed domestically for capital spending & purposes other than the capital expenditure.

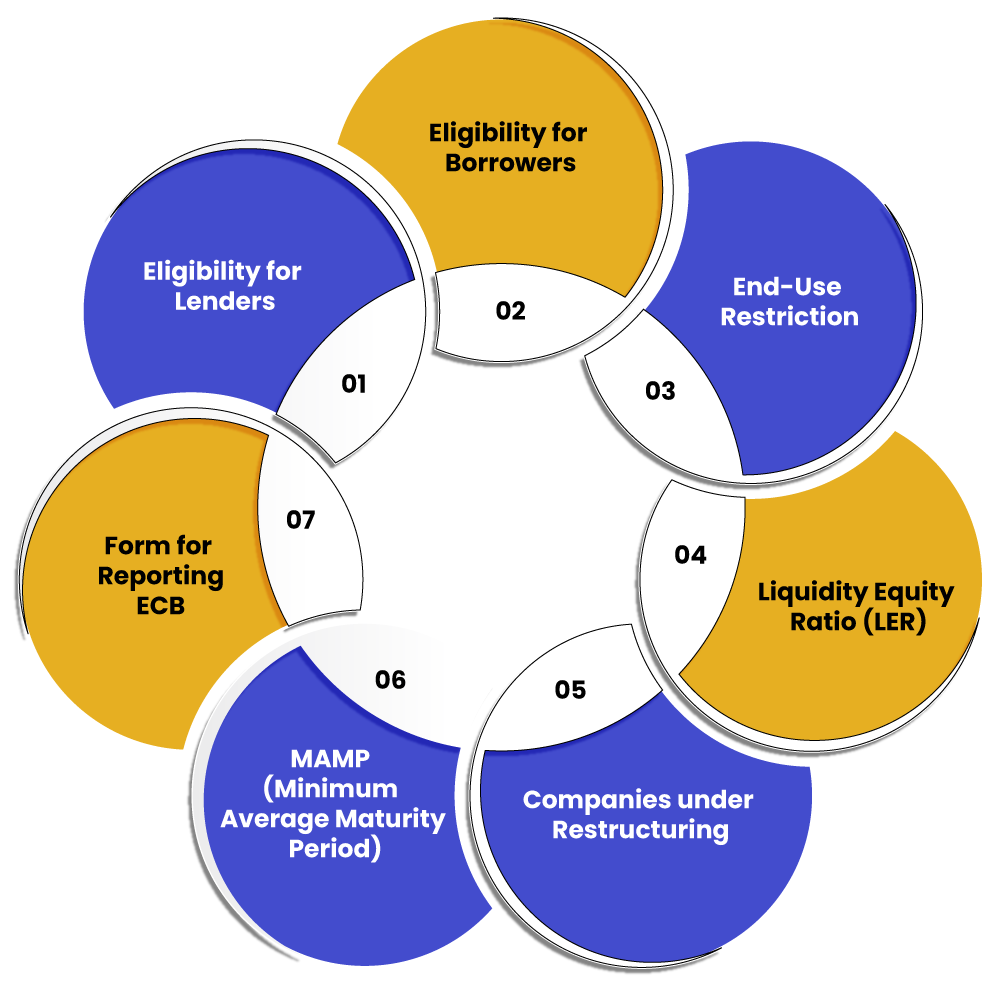

Changes in the New Regulations

- Eligibility for Lenders: Like borrowers, the lenders were also classified into tracks. But, in the new policy, the lenders’ eligibility has been diversified as discussed previously.

- Eligibility for Borrowers: Earlier, the companies are categorised into Track I, II, and III to get ECBs. Now, the policy has been liberalised by permitting companies eligible for FDI to get ECBs. As an outcome, even certain Limited Liability Partnerships (LLPs) are now entitled to get ECB which was earlier not possible.

- End-Use Restriction: Exclusion on drawing of ECBs as we mentioned above in the new framework.

- Liquidity Equity Ratio (LER): The new policy delivers that the ECB Liability Equity Ratio under automatic route cannot surpass 7:1 in the case of foreign currency-denominated ECB raised from a foreign equity holder. But, this situation will not apply if the due amount of all ECB, comprising the present ECB, doesn’t surpass 5 million US dollars or its equivalent.

- Companies under Restructuring: A company facing a corporate insolvency resolution process or under a restructuring scheme can increase External Commercial Borrowings only if the resolution plan explicitly permits it to do so. Previously, it was compulsory to take the approval of the Joint Lender Forum or Corporate Debt Restructuring Empowered Committee.

- MAMP (Minimum Average Maturity Period): MAMP has now been made consistent by prescribing a time of 3 years. But, there can be exceptions in various cases as mentioned below:

- MAMP shall be 10 years in the matter of ECB is raised for working capital or general corporate purposes or on-lending by NBFCs for these purposes;

- MAMP can be 1 year for manufacturing sector companies or entities who raise External Commercial Borrowings up to 50 million US dollars to its equivalent per Financial Year (F.Y.);

- MAMP shall be 10 years in the matter of ECB raised for repayment of Rupee loans served nationally for purposes other than capital expenditure or on-lending by Non-Banking Financial Companies for the same purpose;

- MAMP shall be 7 years in the matter ECB is raised for repayment of Rupee loans availed domestically for capital expenditure or on-lending by Non-Banking Financial Companies for the same purpose;

- MAMP shall be 5 years if ECB[1] raised from foreign equity or general corporate purposes or on-lending by Non-Banking Financial Companies for working capital or general corporate purposes.

- Form for Reporting ECB: Earlier, Form 83 was submitted for reporting ECB, whereas now Form ECB needs to be submitted to report ECB in case they require raising funds through the consent route.

Conclusion

External Commercial Borrowings is one of the rising sources for getting foreign capital to India. With the beginning of a new framework that is Master Directions issued by the Reserve Bank of India, the norms have been relaxed substantially, which has improved the effortlessness of doing business in India. Provisions of the automatic route, increased possibility for eligible borrowers & lenders, simpler categorisation of ECBs, regularising delays by submitting late fee reduced hedging necessities, etc., will confidently prove to be a benefit for the economy in the future. This will aid to develop resident companies, which will enhance the economy ultimately.

Read our article:RBI Announces Guidelines to Implement its Circular on Opening of Current Accounts by Banks