Investigation Under Section 11C of the SEBI Act – An Overview

Karan Singh | Updated: Aug 31, 2021 | Category: SEBI Advisory

SEBI was established as a statutory regulatory body on February 21, 1992. It controls and monitors the Indian capital & securities market while ensuring to safeguard the investors’ interests, formulating guidelines and regulations. The head office of SEBI is in Mumbai, and apart from Mumbai, the organization has various regional offices across the country, including Chennai, Ahmedabad, New Delhi, and Kolkata. On the 4th of April, 1992, the Ordinance was cancelled, and SEBI was accorded with legal powers with the passing of the SEBI Act, 1992 by the Parliament of India. In this blog, we will discuss the functions of SEBI, Provisions under Section 11C of the SEBI Act.

Table of Contents

Establishment and Powers of SEBI

Before we discuss the provisions under Section 11C of the SEBI Act, it is vital for you to understand the establishment of and Powers or functions of SEBI in India. SEBI was introduced to observe or monitor unfair practices and to safeguard investors from them. The SEBI is the sole regular of the securities markets of India. Its preamble explains its primary function to protect the investors’ interests in securities & encourage the improvement of and control the securities markets & for matters associated therewith or incid thereto.

The organization was established to fulfil the requirements of all the following groups:

- Intermediaries: SEBI gives a platform to this group and struggles to provide intermediaries with a specialized and competitive market.

- Issuers: SEBI works to furnish investors with a marketplace where they can raise funds smoothly & fairly.

- Investors: SEBI also protects the investors and delivers them with correct details about the companies pertinent in public domains and aids the investors take informed investment decisions & make the market transactions secure.

Management of the Board

- The Board consist of the following members:

- A Chairman;

- Two members from amongst the authorities of the Ministry of the Central Government dealing with Finance;

- One member from amongst the authorities of the Reserve Bank of India (RBI);

- Five other members of whom a minimum of three shall be full-time members to be appointed by the Central Government.

- The General Superintendence, management & direction of the Board’s affairs shall vest in a Board of Members, which may exercise all powers & do all acts and other things which may be exercised or done by the Board.

- Save as otherwise concluded by regulations, the Chairman of the Board also have the powers of General Superintendence and direction of the Board’s affairs and may also implement all controls and do all acts & things which may be implemented or done by the Board.

- The members and Chairmen of the Board referred to in Clauses (a) & (d) of sub-section (1) shall be appointed by the Central Government & all members of the Board referred to in Clauses (b) & (c) of that sub-section shall be nominated by the Central Government and the RBI respectively;

- The other members and the Chairman referred to in Clauses (a) & (d) of sub-section (1) shall be persons of capability, integrity, and standing who have shown ability in dealing with issues concerning the securities market or have special awareness or expertise of law, finance, accountancy, economics, administration or in any other things which in the Central Government’s opinion, shall be useful to the Board.

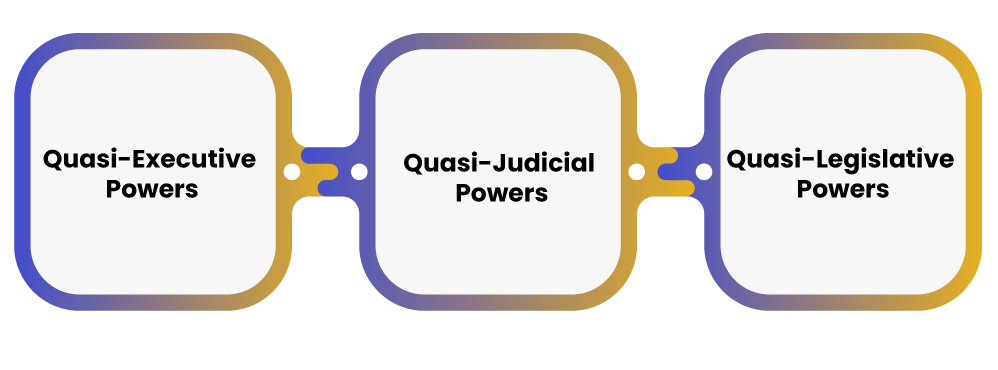

Powers of SEBI:

- Quasi-Executive Powers: Securities and Exchange Board of India has the power to examine the books of accounts & other vital documents to collect or spot evidence of infringements or violations. The authority, as mentioned above, makes it easier to maintain accountability, clearness, and equality in the securities market.

- Quasi-Judicial Powers: This Board has the power to issue judgements in the case of securities market fraud and unprincipled practices. If it determines someone breaking the rules, the regulatory body has the authority to apply rules, pass judgements, & pursue statutory action against the violator.

- Quasi-Legislative Powers: The trustworthy body has been entrusted with the power to develop applicable rules & regulations to safeguard the investors’ interest. Vital disclosure necessities, Listing Obligations, and insider trading prohibitions are some common examples of these policies. The SEBI establishes such rules & regulations to eliminate securities market offences.

SEBI Act- Section 11C of the SEBI Act

The Act gave SEBI the authority to control the capital market, not just to observe but also to implement the guidelines & twin goals of the SEBI Act, namely, the protection of interests of investors and the organized development of capital markets in India. The SEBI Act controls the following sections:

- Members of the Securities and Exchange Board of India Board of Directors, their composition, and their actions;

- The roles & responsibilities of the Board are outlined in the SEBI Act;

- The funding sources, which comprise donations from the Union Government.

- Legal channels & sanctions are governed by these rules.

Provisions under Section 11C of the SEBI Act

Section 11c of the SEBI Act talks about the investigation, and these investigations are conducted to collect evidence of suspected securities market violations like insider trading, price tampering, artificial market formation, public issue related irregularities, and other misconduct, as well as to recognize the companies or individuals accountable for these violations & irregularities. Investigate powers of the SEBI are broad, and even before an inquiry is started, it can result in strict civil & criminal penalties; Over the year, the Board has begun its investigating efforts.

The SEBI under Section 11C (1) can direct a person to investigate the affairs of such intermediary or anyone affiliated with the securities market at any time by writing an order if the Board has grounds to believe that market securities transactions are being handled in a way that is dangerous for securities market or shareholders or the securities market, or if any mediator or an individual associated with the securities has infringed any of the provisions of SEBI Act.

Under Section 11C of the SEBI Act {11C(2), 11C(3)}, all registers, books, other documents and records of, or relating to the company should be maintained & produced to the Investing Authority, or any individual certified by it on their behalf, by every office, employee, director of the firm or anyone associated with the securities market. The Investing Authority will have the authority to maintain the records with them for six months and can call for the records again from the intermediaries described under Section 12 if the Investigating Agency requires the documents again.

Impounding of Documents – Section 11C of the SEBI

If the investigating authority has substantial grounds to believe that the mediator in control of the document can alter, destroy, or hide the records from the authority. The Investigating Authority can apply to the Court or magistrate for an order impounding the documents, and the investigation authority is permitted to keep the confiscated documents with them until the investigation is completed.

Exemption

Unless a company engages in market management or insider trading, a judge, a magistrate, or Court cannot order the seizure of books & other documents of a listed public company or a public company (other than the intermediaries listed under Section 12) that aims to get its securities listed on any recognized stock exchange.

Examination on Promise – Section 11C of the SEBI Act

In Section 11C of the SEBI Act, a director, management, employee, or intermediary of the company can be questioned under-promise by the investigation agency. The agency may take notes on the examination & have the individual examined sign it so that it can be used against them as evidence. It necessitates the personal appearance of the individual before the investigative agency.

Punishment under the Section 11(C) of the SEBI Act

Suppose a director, management, intermediary, or employee of the company fails to provide information, reports, or documentation that they are required to be produced or fails to contribute personally before an investigation agency or sign examination notes. In that matter, they will have to face imprisonment for up to one year, or a fine of up to Rs. 1 crores or both as well as a fine of up to Rs. 5 lakhs per day during which the failure continues.

Investigation under the Section 11C of the SEBI Act – Case Study

- Adjudicating Officer (AO) vs Mahesh Kumar Patel (MKP) (2005)

Details

In this matter, SEBI started an investigation in the year 2004 into the unexpected growth in the process of SSPL (Sword & Shield Pharma Limited) within a short duration. On 2nd June, 19th July, 9th & 23rd August, letters were issued to Mahesh Kumar Patel, the petitioner associated with the investigation under Section 11C of the SEBI Act. The petitioner didn’t show up for their hearing with the Investigating Authority. Adjudication processes were commenced in response to the claimed non-compliance with the summons of the SEBI.

Problem

The petitioner alleged that he didn’t come under the scope, range, and jurisdiction of SEBI because he was not a registered intermediary of the SEBI. In response to the SEBI’s letter, the petitioner claimed that Aarushi Consultancy, of which he was the owner and has received an identical letter from SEBI in a similar case. He has already submitted the details required by SEBI, and he didn’t & was not required to submit any other information or details.

Judgement

The petitioner is a participant in the securities market, as he is the only owner of Aarushi Consultancy, and he is also a regular trader in the stock market, as represented by their own Demat Account[1]. So his argument that he didn’t come under the jurisdiction was incorrect, and SEBI, under Section 11C (3), has the authority to call a mediator or any individual affiliated with the securities market to provide information to the investing authority & as an individual in the securities market, he was expected to provide all information to the Investigating Authority that was needed or considered vital for the investigation of the agency. He was not able to prove that the details he was asked for were identical to what Arushi Consultancy required. The primary presumption of the petitioner was that whatever Aarushi Consultancy had provided would be sufficient for the summons he had received.

By not giving the response to the summons & failing to appear before the Investigating Authority (IA), he refused the IA the chance to get clarifications or extra information from him, which he would have been capable of providing as the owner of Aarushi Consultancy and which couldn’t be conveyed via written submissions of the Aarushi Consultancy.

- Secretary, Government of India & Others vs Mitesh Manubhai Sheth (1997)

The High Court of Gujarat in favour of the right of the broker to be shown by a lawyer. The Court decided that having a lawyer present is useful not only to the criminal but also to the tribunal or inquiry committee in reaching a just & appropriate verdict. Now, it is accepted that, in a matter involving a judicial, quasi-judicial, or even administrative decision that affects the legal rights of an individual, the party affected should be allowed to be protected by a lawyer if the facts of the case merit it.

Conclusion

After discussing the provisions under Section 11C of the SEBI Act, it is concluded that investigations of the SEBI had a positive impact on the financial market over the past years. The SEBI’s investigations, together with standard surveillance methods, have decreased the number of claimed market manipulations & price rigging cases. A range of administrative and punitive proceedings was taken under the SEBI Act and the various EBI Rules & Regulations. Money penalties, cautions, suspension of activities & suspension of registration, limiting dealing in equities & access to the equity market, asking trustees and key individuals of mutual funds to resign for failing to safeguard the investors’ interests.

Read our article:Examine the Problems Arising From the Usage of AI in M&A Due Diligence