A Complete Guide on Terrorist Financing and Money Laundering for NBFCs

Karan Singh | Updated: Mar 24, 2021 | Category: NBFC, RBI Advisory

The RBI or the Reserve Bank of India has issued a notification for a modification to Master Director on KYC wherein the regulated companies must occasionally carry out Terrorist Financing and Money Laundering for NBFCs risk assessment activities, and the first assessment is mandatory to be carried out by June 30, 2020. Scroll down to check more information regarding Terrorist Financing and Money Laundering for NBFCs.

Table of Contents

Understand the Idea of Terrorist Funding and Money Laundering Risk Assessment

This idea arises from the recommendations of the FATF or Financial Action Task Force. It has offered detailed guidance on Terrorist Financing and Money Laundering risk assessment, and it is specially made for current NBFCs (Non-Banking Financial Companies). Terrorist financing is a risk that functions via consequences and susceptibility. It is mentioned as a non-legitimate method of fundraising for Terrorist Organizations.

Also, Read: Operational Manual of the NBFCs: A Complete Guide

What is the Procedure of Risk Assessment by NBFCs?

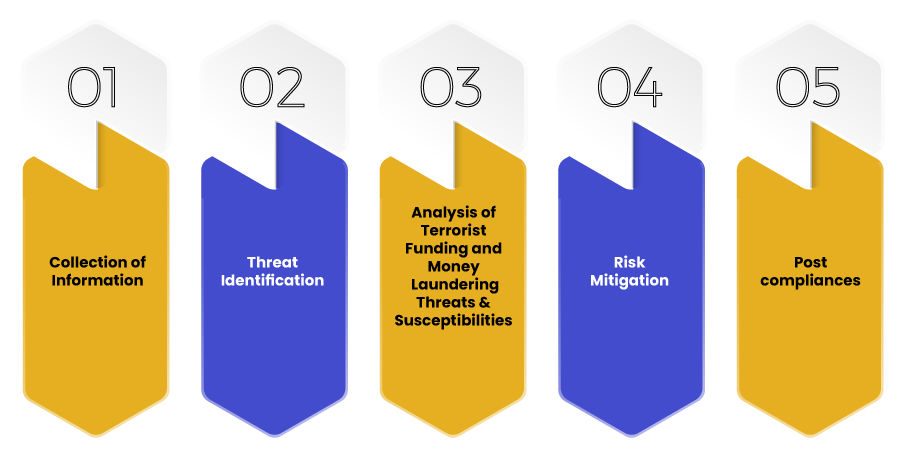

The procedure of Risk Assessment by Non-Banking Financial Companies does not require to be complicated, but it must be proportionate with the nature and size of its business. A simple risk assessment if enough for especially less difficult Non-Banking Financial Companies. The process of the risk assessment process by Non-Banking Financial Companies based on the guidelines of FATF principles are divided into the following phases:

- Collection of Information: The procedure of risk assessment by NBFCs starts with collecting the information on various variables like information of the commoncriminal environment, terror threats and financing, etc. Such information can be collected internally or externally. The Directorate of Enforcement deals with the matters of terrorist financing and money laundering in India. It has detailed information and the terrorist list. Furthermore, the information can also be availed from the CBI or Central Bureau of Investigation.

- Threat Identification: once they collected all the information, the jurisdiction and the sector-specific threats must be identified on the basis of such collected information. Although the treat identification should be based on the domestic/national level, it should not be restricted to it only. It should be associated with the nature and size of the business entity. The Non-Banking Financial Companies should look at the controls that are located, including the quality of Risk Management Policy, working of internal functions, etc.

- Analysis of Terrorist Funding and Money Laundering Threats & Susceptibilities: In this procedure, it should be known how the identified threats are going to affect the entity or organization. Some factors like scale, complexity, nature, and diversity of their business should be considered during the risk assessment. Apart from this, the governing findings and the internal audit must also be considered. The size and capacity of its transaction must be kept in the picture during the risk assessment. The Non-Banking Financial Companies should complement this information with the information received from external sources and internal sources.

- Risk Mitigation: Once the threats and vulnerabilities are analyzed or examined, the Non-Banking Financial Companies are required to progress and implement policies to mitigate the risks associated with Terrorist Financing and Money Laundering. The process of CDD or Customer Due Diligence should be informed to recognize and identify by their customers by requiring them to gather information on their profession and the need for financial services by them:

- Customer Due Diligence Procedures: Starting the procedure for Customer Due Diligence (CDD) is the first step while starting with the customer relationship. This procedure identifies a customer, and acustomer’s risk-based assessment is conducted. CDD procedures should also include checkpoints with regards to Terrorist Financing and Money Laundering. The activity of a customer or business’s nature is also understood in the procedure of Customer Due Diligence. Misuse of a legal person for conducting Terrorist Financing and Money Laundering must be prevented by taking some measures.

- Ongoing Observing and CDD: Ongoing observing is the examine of the transactions to know if the transactions are reliable with the Non-Banking Financial Companies customer’s knowledge and the loan product’s nature and business relationship. Observing can help in identifying doubtful transactions.

- Reporting: The Non-Banking Financial Companies must mark the unfamiliar movements of funds for analysis, and there should be a case management system so that such type of funds are examined timely, and it can be determined if the funds or the transactions are mistrustful. Those funds that are suspicious should be reported to the Financial Intelligence Unit or FIU in the manner stated by the authorities.

- Internal Control: For proper risk alleviation, it is vital to have satisfactory internal controls. These internal controls include governance arrangements where the responsibility for CFT and Anti-Money Laundering is clearly assigned, and proper omission is in place to examine the usefulness of Non-Banking Financial Company policies and processes to identify the monitor risk and assess.

- Training and Recruitment: Non-Banking Financial Companies must make sure that the employees that they hire have honesty and are highly skilled enough, and own the expertise and the understanding to perform their functions. The employees and the worker should be trained to assess the quality of Non-Banking Financial Companies Terrorist Financing and Money Laundering Risk Assessments. Sufficient training shall help them to form sound judgments concerning the capability and the proportionality of the Anti Money Laundering controls.

- Post Compliances: After completing the assessment, the risk impact must be recorded, and measures to alleviate the risks must be provided. The information founding the basis of the risk assessment process and must be updated from time to time; where there is an important change in the information, the risk assessment process should be carried out.

Conclusion

The compliance officer of Non-Banking Financial Company must be given the authority, right, resources so that the tasks can be carried out with his knowledge, consisting of access to all the related internal information. Only then productivity can be actually brought out, and the risk of money laundering and terrorist financing can be alleviated. Non-Banking Financial Companies should take some steps so that they are satisfied with their CFT or AML policies, and regulators are followed.

Also, Read: What are the Major Challenges and Remedies by NBFCs? – An Overview