Amendment in Form SH-7 by the Ministry of Corporate Affairs

Shivani Jain | Updated: Jan 18, 2021 | Category: News

Recently, the MCA (Ministry of Corporate Affairs) has used its powers given under the provision of section 143 (11) of the Companies Act 2013 and issued a Notification No. G.S.R. 794(E), dated 24.12.2020, concerning the Amendments made by it in Form SH-7. Further, the said amendment was made under the Companies (Share Capital and Debenture) Rules 2014.

Moreover, from now onwards, these rules will be known as the Companies (Share Capital and Debenture) Second Amendment Rules 2020 and will come into force from the date of its publication in the Official Gazette.

In this blog, we will talk about the concept and the amendment in Form SH-7 made by the MCA.

Table of Contents

Concept of MCA Form SH-7

The term MCA Form SH-7 denotes a statutory form, which a company needs to file within 30 days from the alteration made in the Authorised Capital. Further, such a form is filed with the Registrar of Companies (ROC), together with the fees prescribed.

Governing Laws for Form SH 7

The governing laws for MCA Form SH 7 are as follows:

- Section 64 of the Companies Act 2013;

- Rule 15 of the Companies (Share Capital and Debenture) Rules 2014, now known as Companies (Share Capital and Debenture) Second Amendment Rules 2020;

Situations that Require Filing of MCA Form SH 7

The situations that require filing of MCA Form SH 7 with the ROC are as follows:

- Independent Increase in the Share Capital;

- Increase made in the Share Capital after Passing of an Order by the Central Government;

- Redemption of Preference Shares by the Company;

- Consolidation of the Total Number of Shares;

- Division of the Total Number of Shares;

- Increase in the number of Members of the Company;

Amendment in Form SH-7

Earlier, as per section 64 of the Companies Act 2013, the above mentioned situations require the filing of Form SH 7 with ROC (Registrar of Companies). However, the MCA has amended section 64 by inserting clause (e) in sub section (1), which is as follows:

“(e) Cancel Shares which, at the date of the passing of the resolution on that behalf, have not been taken or agreed to be taken by any other person, and diminish the amount of its share capital by the amount of the shares so cancelled.”

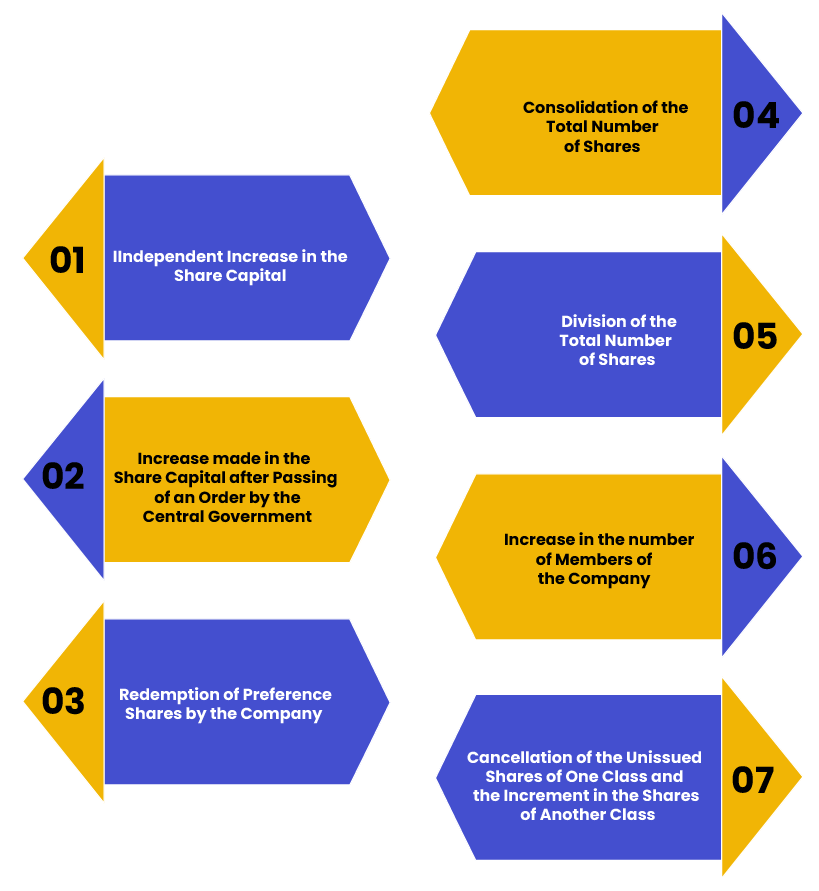

That means now the situations under which there is a need to file Form SH 7 with the ROC are as follows:

- Independent Increase in the Share Capital;

- Increase made in the Share Capital after Passing of an Order by the Central Government;

- Redemption of Preference Shares by the Company;

- Consolidation of the Total Number of Shares;

- Division of the Total Number of Shares;

- Increase in the number of Members of the Company;

- Cancellation of the Unissued Shares of One Class and the Increment in the Shares of Another Class;

Conclusion

In a nutshell, the MCA by way of its Notification No G.S.R. 794 (E), dated 24.12.2020, has amended the purposes for which there is a need to file MCA Form SH 7 with the ROC. The same was done by inserting (e) in sub section (1) of section 64 of the Companies Act 2013[1].

The main reason behind the same was to increase the scope and ambit of section 64 (1), under which Form SH 7 is filed. Also, from now onwards the Companies (Share Capital and Debenture) Rules 2014will be known as the Companies (Share Capital and Debenture) Second Amendment Rules 2020.

For any other detail or query, reach out to Swarit Advisors, our skilled experts are there to cater to all your doubts concerning Company Law.

Also, Read: Companies (Compromises, Arrangements & Amalgamation) Second Amendment Rules 2020