What are the Pros and Cons of Non Convertible Debentures (NCD) Issued by NBFC?

Japsanjam Kaur Wadhera | Updated: Feb 02, 2021 | Category: NBFC

Non- Convertible Debentures (NCD) are the fixed income instruments, which are issued or obtained by the high rated companies in the form of the public issue to reserve long term capital appreciation. NCD relatively offer high rate of interest as compared to convertible debentures. Non- convertible debentures are the popular method of raising funds for the NBFCs. The NCDs permits the investors to reserve their funds for a long time at a higher interest rate. Also, the guidelines of the Reserve Bank of India have, to a great extent tightened the NCDs and raising other forms of money of NBFCs. This article will provide with you with the information regarding what are the pros and cons of Non- Convertible Debentures (NCD) issued by NBFC.

Table of Contents

What are Non Convertible Debentures (NCD)?

According to the guidelines of the Reserve Bank of India (RBI), Non- Convertible Debentures are secured negotiable money market instruments or debt instrument which are matured in less than one year issued by the NBFCs and corporates to meet with their short- term funding requirements, issued by way of private placement with the investors. The guidelines also cover Non Convertible Debentures which are matured over more than one year with optionality attached to it which can be exercised within a year from the date of the issue.

NCDs are the financial instruments used by the NBFCs and companies to raise long-term capital and this action is performed by them through public issue of shares. Basically, Non- Convertible Debentures are debt instrument. The NCDs have a fixed tenure and the people receive a regular certain rate of interest on the investment made by them.

Some debentures can be converted into shares at one point of time and this is done at the discretion of the owner. However, it is not possible in the case of non- convertible debentures. And that is why, they are known as non- convertible debentures or NCDs.

The Non- Banking Financial Companies (NBFCs) raises money by way of debt security or by issuance of capital, including debentures through private placement or public issue. Therefore, there has been witnessed an increase in the borrowings of the NBFCs through the issue of debentures majorly being on private placement basis. And hence, NBFCs depend on NCDs.

Conditions to Issue NCDs in NBFCs

The following are the conditions which are required to issue NCDs in NBFCs:

- It is necessary to disclose the financial position of the company to the prospective investors as per the standard market practice.

- The company further is required to provide a certified copy of the investors to the investors by assuring that it has complied with all the eligibility criteria laid down by the RBI.

- It is mandatory for the company to comply with all the provisions of the Companies Act, 2013 and the regulations framed by the Reserve Bank of India (RBI).

- The company shall be issued with the debenture certificate within the prescribed period specified in the Companies Act, 2013.

- The Non- Convertible Debentures issued at the face value carrying a coupon rate or a discount rate to face value as a zer0 coupon instruments is determined by the corporate.

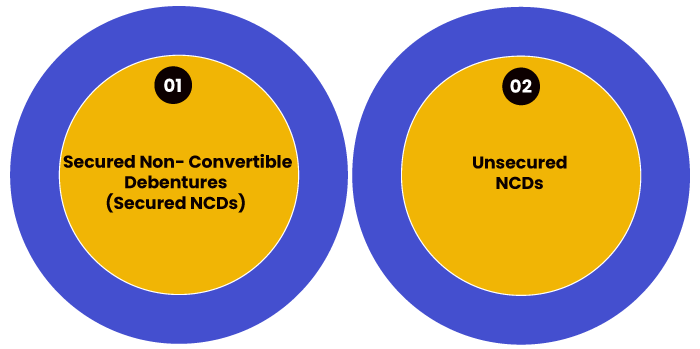

What are the types of Non- Convertible Debentures?

There are two types of Non- Convertible Debentures, which are as follows:

Secured Non Convertible Debentures

The secured NCDs are comparatively safer of the two kinds of NCDs as the issues of such type are backed by the assets of the company. If at any timecompany fails to pay, then the investors can recover their dues by liquidating the assets of the company. However, the interest offered on secured NCDs is low.

Unsecured NCDs

The unsecured NCDs are riskier than the secured NCDs as it is not backed by the assets of the company. Therefore, when at any time company fails to pay, the investors are left with no choice but to wait until they receive the payments as no assets of the company can be used to recover their dues. However, the rate of interest offered by the unsecured NCDs is higher as compared to the secured NCDs.

Also, Read: Know the Factors which led to the growth of Indian NBFCs

Pros and Cons of Non- Convertible Debentures

The pros and cons of non- convertible debentures are as follows:

Pros Non Convertible Debentures

- Every NBFC or company that seeks to raise money through Non- Convertible Debentures (NCD) is rated by the agencies such as CRISIL, Fitch Ratings, CARE and ICRA. Therefore, the information provided is absolutely verified and there are zero chances of fraud.

- The fact that the NCDs issued by the NBFC are regulated closely by the Reserve bank of India (RBI), it benefits the investors. The rate of interests keeps on fluctuating on the other investments and therefore, in these circumstances the NCDs offer a good instrument to keep the returns for a longer period of time.

- Non- Convertible Debentures issued by the NBFCs normally pay the rate of interest of 150- 175 basis points higher than what is paid by the banks on their FDs. And since, most of the NBFCs issuing NCDs are well capitalized and reputed, investors do not see much risk in investing in them.

- The debentures have a first or second charge n the assets of the issuer. Therefore, they are much safer as compared to the other unsecured forms of investment.

- If the rates start falling by 25- 50 basis points from the current level, the investor tends to enjoy the capital appreciation on these NCDs. And hence, this is an advantage.

Cons Non Convertible Debentures

- There are no guaranteed returns beyond the bonds of the government and bank fixed deposits, even bank fixed deposits have risk but it is very low. Therefore, the moment the investors see promises of returns larger than the returns which are offered by the government bonds, they should understand that it will result in facing risk. This is the cardinal or basic rule of investing.

- NCDs are not efficient in the situation of tax. For example, even though 9%- 10% coupon rate is paid by NCD, the actual returns are less than 7% on the post- tax basis.

- Another major risk is inflation. Most of the returns mentioned by NCDs are in nominal terms which provide the right idea regarding the soundness of return. The real return will always be less than the nominal return. Real return means the nominal return minus the inflation. Therefore, if inflation goes up, the real return will go down.

- The are various class of assets in NBFCs. It is divided into two levels that is high quality NBFC and low quality NBFC. The investors must use their discretion and invest accordingly in the NCDs issued by the NBFC only after checking the credit rate of these NCDs. The credit rating is the expert opinion on the issuer’s repayment capacity, and it is advisable to stock the high rated NBFCs only.

Eligibility to Issue NCDs

Any NBFCs or corporates are eligible to issue NCDs on fulfilling the following criteria:

- The NBFC or corporate is having a tangible net worth which is not less than Rs 4 crore in accordance with the latest audited balance sheet.

- The company is endorsed with a term loan or working capital limit by banks or all India financial institution.

- The classification of the company’s account of the borrower is done as Standard Asset by the financial banks or institutions.

Conclusion

There are many pros and cons of the Non- convertible debentures issued by NBFC. Non- Convertible Debentures are suited to the investors who are willing to invest their funds at a high rate of return and who have the ability to take higher risk. Therefore, for many institutional investorsthey prefer NCDs but, for the individuals there may be other profitable investment opportunities available in the market andit depends upon the investor to make the right choice while investing.

Also, Read: NBFC in Insurance Business: How can NBFC Participate in Insurance Business?