SEBI Guidance Note on disclosure of Related Party Transactions

Kandarp Vanita | Updated: May 14, 2021 | Category: SEBI Advisory

Section 188 was enacted under the Companies Act, 2013, which began to regulate few kinds of transactions that occur between companies and its “related parties” and it also provides that if it exceeds a specified monetary threshold then approval by non-related parties of such transactions is required.

It is mandatory for the Companies to follow the requirement of listing regulations and other appropriate regulations that are amended time to time. Hence, SEBI came up with a guidance note on disclosure of related party transactions and in this blog we will know about it in details.

Table of Contents

Who are related parties?

The list of persons and entities that are considered related parties by the law is very long. The Companies Act, 2013[1] states that a related party with respect to a company, means:

- A director and includes a key managerial personnel or their relatives;

- a firm, in which manager, director, or his relative is a partner;

- a private company in which a manager, director or his relative is a director or a member;

- a public company in which a director or manager is a director and is holding more than two per cent of its paid-up share capital together with his relatives;

- anybody corporate whose managing director, Board of Directors, or manager is familiar to act according to the advice, instructions or directions of a director or manager;

Any person on whose recommendation, directions or commands a director or manager is habituated to act.

Any corporate body which is:

(a) A holding, associate or subsidiary company of such company;

(b) A subsidiary of the holding company to which that company is also a subsidiary;

(c) Any investing company and the venture of that company.

What are Related Party Transactions?

The Related Party Transactions shall be entered by the Companies after taking into consideration the following provisions.

Related Party Transactions (RPT) are the transactions that a company does with the parties that are related to it. A company entering into arrangements and contracts with the related party is as follows:

- sale, supply or purchase of any materials or goods;

- disposing, selling or otherwise buying property of any kind;

- leasing of any kind of property;

- availing or render any services;

- appointing any agent for the sale or purchase of goods, services, materials, or property;

- the appointment of the related party to any office or place of profit in the company, its subsidiary company or in the associate company; and

- Underwrite the subscription of the securities or the derivative of the company.

What is the SEBI Guidance?

For Listed Companies:

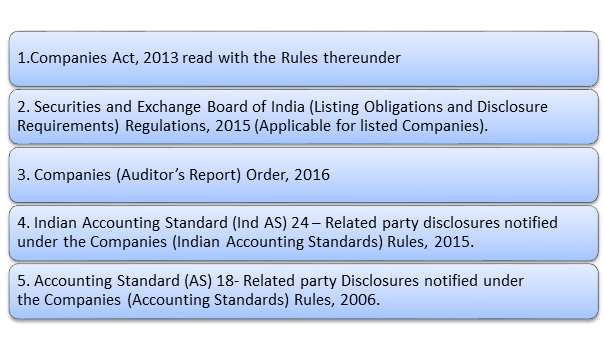

In accordance with the Regulation 2(1) (zc) of SEBI (Listing Obligation and Disclosure Requirement) Regulations, 2015 (“Listing Regulations”): ‘Related Party Transaction’ shall mean that there is transfer of services, or obligations, or resources between any of the listed entity and a related party, despite of whether if there is any price charged and any transaction with the related party shall be considered to include the single transaction and the group of transactions in a contract.

As per Regulation 23(1) of Listing Regulations: A transaction with the related party shall be construed as material if the transaction is entered into either individually or taken jointly with the previous transactions for the duration of the financial year, and goes beyond 10% of the consolidated annual turnover of the listed entity according to the previous audited financial statement of the given listed entity.

In accordance with the Regulation 23(1A) of Listing Regulations: A transaction concerning payments that are made to the related party with reference to the royalty or brand usage shall be construed as material if the transaction are entered individually and also taken together with the preceding transactions during that financial year, exceeding five percent of the consolidated annual turnover of the listed entity in accordance with the previous audited financial statement of that listed entity.

In accordance with the Accounting Standard (AS)–18: ‘Related Party Transactions’ is the transfer of obligations or resources between the related parties, despite of whether the price is charged or not.

As stated by Ind AS-24: Related Party Transactions is a transfer of services, resources or obligations between a related party and reporting entity, despite of whether the price is charged or not.

Reporting & Disclosures

SEBI has specified the reporting and disclosure requirements at different places in the Listing Regulations connected to “Quarterly Compliance Report on the Corporate Governance, where it is required by the listed company to submit the report (in specified format as mentioned by SEBI) to the stock exchange within 15 days from the close of the quarter. The Report shall include the details of ‘all the material transactions with related parties’ and must be signed either by Chief Executive Officer or Compliance Officer

(1) Website: Regulation 46 of Listing Regulations says that the listed company is mandated to maintain a functional website that shall contain the essential information and the website will propagate “Policy on dealing with the Related Party Transactions”.

(2) Corporate Governance Report: In the corporate Governance Report which is included in the Annual Report, the company is obligated to disclose the ‘materially significant’ RPT’s that may have impending conflict with the benefit of listed entity at large. The corporate Governance Report shall also give a web link with reference to the policy on dealing with RPTs.

(3) Annual Report: with respect to Regulation 53 of the listing Regulations, the Annual Report shall contain the RPT disclosure on

(4.1) Holding Company

(4.2) Subsidiary Company

Conclusion

The SEBI Clause 49 has certain regulatory requirements for the related party transactions. Hence, related party transactions shall include the transfer of resources/services/obligation and has to be approved by the shareholder by passing a special resolution. Therefore, the rules of SEBI must strictly be observed as non compliance of the same attracts penalties.

Read our article:Preferential Allotment of Equity Shares: A Complete Guide