What are the Differences Between Closed and Semi-closed Wallet?

Karan Singh | Updated: Aug 13, 2021 | Category: Prepaid Wallet

A digital wallet is also recognised as an e-wallet, and it is a software-oriented system that protects the payment details and passwords of the clients or customers for different online payment methods and websites. Using an e-wallet or digital wallet allows customers to complete purchases easily and rapidly with near-field communications technology. Digital wallets can be used in connection with mobile payment systems, which permit clients or users to pay for purchases with their mobile phones. An e-wallet can also be used to store digital coupons & information. There are three different categories of digital wallets that are an open, closed and semi-closed wallet. To provide such services to customers, one has to obtain Prepaid Wallet License from the Reserve Bank of India. Scroll down to check the differences between closed and semi-closed wallet.

Some important points to remember

- E-wallet mentions to a financial instrument that allows end-user to store funds, receive or make payments and keep a view on the payment histories;

- These financial tools cum software may be registered in the mobile application of the bank, such as Google pay, PhonePe, or PayTm.

Table of Contents

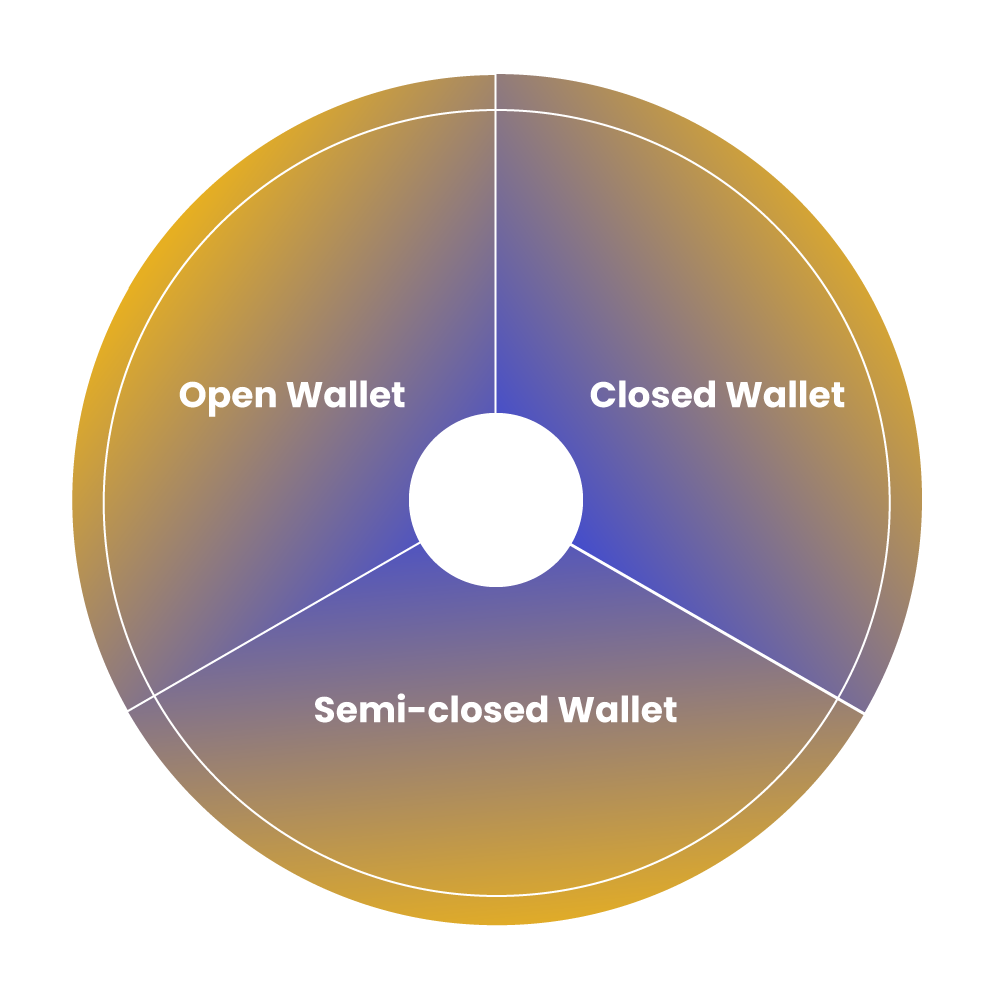

What are the Types of Digital Wallets or E-Wallets in India?

Before we discuss the differences between closed and semi-closed wallet, let’s first understand the types of digital wallets in India:

- Open Wallet: Banks or institutes associated with banks issue open wallets. Customers with these wallets can use for transactions allowed with a semi-closed wallet in addition to withdrawal of funds from banks and TMS & Transfer of Funds. Some examples of open wallets are Master Card, Visa Card, etc.

- Closed Wallet: An entity selling its products and/or services can develop a closed- wallet for clients. Customers of a closed wallet can use the funds stored to make transactions with only the issuer of the wallet. The money from returns, cancellations or refunds is collected in the wallets. For example, Amazon Pay is a closed wallet.

- Semi-closed Wallet: It grants customers to make a transaction at listed locations and merchants. Although the coverage area of semi-closed wallets is restricted, both offline and online buying can be done through these wallets. However, merchants need to sign agreements or contracts with the issuers for accepting payments from mobile wallets. Examples of semi-closed wallets are Paytm, Freecharge, Mobikwik, etc.

Following are some advantages of open, closed and semi-closed wallet in India:

- Open Wallet:

- It can be used for cash withdrawal;

- Used for the buy goods or products by swiping cards;

- Used for mobile banking and internet banking.

- Closed Wallet:

- Receive cashback and refunds;

- Purchasing products and services.

- Semi-Closed Wallet:

- Used to buy goods from affiliated merchants;

- Money transfer among wallets’ holders.

Differences between Closed and Semi-Closed Wallet

Following are some critical differences between closed and semi-closed wallet:

- In semi-closed wallets, one can do digital shopping and send money to the recipient in the same wallet network. Such a wallet also allows customers to transfer an amount of wallet balance to their legal bank account;

- A closed wallet is a platform-specific wallet service provided by the service providers to their clients or users. It is primarily used by online-based companies to acquire a loyal user base. It enables clients to make quick payments and earn cash backs;

- Semi-closed wallets are broadly used in India owing to their incomparable resilience and extensive applicability. Semi-closed wallets like PayTm, Oxygen, Citrus, etc., are the best examples of this wallet. The RBI consent is compulsory for commencing a semi-closed wallet service in India;

- A closed wallet has restricted applicability, and it provides a restricted pool of clients. A perfect example of this wallet is the Amazon wallet or Myntra Wallet. It is essential to remember that this wallet does not provide benefits like cash withdrawal or redemption to the clients;

- The idea of digital wallets is not new for customers in India. These services find their way into the Indian market around a decade back, and since then, it has been protected a massive pool of customer. E-wallet is insistently used in the e-commerce industry and has become a feasible alternative to payment banks;

- An open, closed, and semi-closed wallet can be used to transact offline and online, which comprises availing online services, purchasing products online, getting financial services, paying fees, etc. through or to the merchant which have a legitimate contract with the issuer to accept payment instruments;

- Since such wallets are controlled by different agencies other than banks, they must send this money to the escrow account with an associate bank. Interest applicable to such deposits varies in accordance with the agreement terms between the payment company and the bank.

The prepaid payment instrument[1] is categorised into 4 categories, and you can check the same below:

- Open Payment Instrument;

- Semi-open Payment Instrument;

- Closed Payment Instrument;

- Semi-closed Payment Instrument.

Closed payment instruments mention the payment tools basically bestowed by the businesses for use at their establishment only. These instruments don’t provide services like redemption or cash withdrawal. Ola Money, Freecharge credit comes in this category.

These tools are repayable at recognised merchant locations that contract, especially with the issuer, to accept the payment instrument. Moreover, these tools don’t permit cash withdrawal/redemption by the owner. Following is the detailed comparison between closed and semi-closed wallet:

| Closed Wallet | Semi-Closed Wallet |

| It can be used to receive funds and cashback to buy only from the issuer merchant to pay the seller of the issuer merchant. | This wallet can be used to pay associated merchants against products and services purchased. To buy products and services from the issuer to transfer funds between customers. |

| Authorisation of the Reserve Bank of India or PPI (Prepaid Payment Instruments) License is not mandatory for customers seeking to influence closed wallets. | Banks can work without a Prepaid Payment Instruments License. However, the same is not correct with non-bank companies. |

| Interoperability is not valid on this wallet. | Interoperability is allowed only for complete KYC semi-closed wallets. |

| Given individual to merchant spending, the transaction is closed wallet only exists between issuer and wallet owner. | Permitted only with contracted merchants. |

| Cash withdrawal is not possible for the customers of this wallet. | Cash withdrawal is not possible in this wallet. |

| Not clearly prohibited. Permissibility is not clear and will depend on the transaction type. | Permitted for complete KYC semi-closed wallet is not for minimum KYC semi-closed digital wallets. |

| This wallet cites to a digital wallet permitted to a company to customers for purchasing products and services from that company. For e.g., Clear trip, Amazon. | This wallet can be used to buy products and services, as it’s a payment instrument that is redeemable at recognised merchant locations that contract, especially with the issuer, to recognise the payment instrument. |

Conclusion

After discussing the differences between closed and semi-closed wallet, it is clear that it serves different purposes where the transaction under closed wallets occurs between the issuer and the wallet owners only, whereas the semi-closed wallet permits their users to transact money through issuer as well as associated merchants.

Read our article:RBI Mandates Interoperability of PPIs (Pre-paid Cards, Wallets)