Tax Audit under Section 44AB of the Income Tax Act, 1961

Khushboo Priya | Updated: Apr 17, 2019 | Category: Income Tax

Tax audit is a mandatory inspection done by the practicing Chartered Accountant to ensure the details of the income provided by the taxpayer are accurate. As per Section 44AB of the Income Tax Act, 1961, the tax audit of an entity is imperative. If any business or professional under certain prescribed categories don’t undergo the audit, the entity would be subject to a hefty penalty.

Therefore, in this blog, we are going to cover several aspects of a tax audit under section 44AB of the Income Tax Act, 1961. Let’s start with the definition.

Table of Contents

What is a Tax Audit ?

Tax Audit is an examination conducted to inspect and verify whether the income of the assessee and the claim for deductions are accurate. Generally, it’s the process of verifying the books of accounts of the taxpayer to validate the correctness of the income tax and compliance with Income Tax Law.

At the time of preparing the books of accounts, the assessee must comply with the provisions of Income Tax Act, 1961, specifically from Section 28 to Section 44DB.

Principal objectives of Tax Audit

Tax audits are conducted to obtain the following objectives:

- One of the primary goals of this audit is to obtain a report as per the requirements of Form no. 3CA [1] , Form no. 3CB [2] and Form no. 3CD [3] .

- Another objective of this audit is to ensure that the records and books of accounts of the taxpayer are properly maintained as indicated in the taxpayer’s income.

- Reporting of discrepancies or observations noted by the tax auditor after a methodical inspection of books of accounts.

- To report required information such as compliance of several provisions of income tax law, tax depreciation, etc. As a result, it lets as well as saves the time of the tax authorities in examining the correctness and accuracy of the income tax return such as total income, claims for the deduction, and more filed by the taxpayer.

- Such audits are also performed to find and avoid any kind of fraudulence.

Who conducts tax audit under section 44AB?

Only a Chartered Accountant who is in full-time practice and possesses a certificate of practice can conduct the audit under section 44AB. A chartered accountant carries out a methodical inspection of books of accounts as per the formats provided by the department.

Types of accounts that fall under this audit

I have enlisted below the types of accounts that come under the audit:

- Company account

- Individual/Proprietorship

- Partnership Firm

- Association of person

- Local authority

- HUF (Hindu Divided Family)

What is Tax Audit Limit?

Under Section 44AB of the Income Tax Act, 1961, the tax audit limit for businesses, professionals and presumptive taxation scheme are as follows:

|

Entity |

Tax Audit Limit |

|

Business | Tax audit is applicable to businesses with gross receipts or total sales turnover exceeding Rs. 1 crore in the earlier assessment year. |

|

Profession | Profession or professional with gross receipt more than Rs. 50 lakhs in any of the earlier assessment year. |

|

Presumptive Taxation Scheme | If the entity is registered under the Presumptive Taxation Scheme and the total sales turnover surpasses Rs 2 crores, then tax audit is mandatory. |

Business: Under the Income Tax Act, 1961, the term business means any economic activity that has some profits and gains. However, according to Section 2 (3), a business could be a trade, manufacturing activity, commerce, or any concern or adventure in the nature of commerce, trade, and manufacture.

Profession: According to Rule 6F of the Income Tax Act, 1961, a profession could be any of the below-described entities:

- Architect

- Accountant

- Engineer

- Interior Decorator

- Technical Consultant

- Film Artists such as Director, Actor, Editor, Singer, etc.

- Authorised representative

- Legal Professionals

- Medical Professionals such as Doctor, Physiotherapist, etc.

Presumptive Taxation Scheme: If the total turnover of a person registered under the Presumptive Taxation Scheme under Section 44AD increases, then a tax audit is mandatory. Moreover, if the registered person claims that the profits of the business are lower than the profit calculated, then as per the Scheme, a tax audit is compulsory.

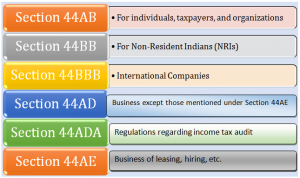

Types of Tax Audit in India

As per the provisions of Income Tax Act, 1961, there are six types of Tax Audit in India:

Section 44AB

Under section 44AB of the Income Tax Act, it is necessary for the following entities to get the tax audit conducted:

- Any business or company whose gross receipt or total turnover crosses Rs. 2 crores in any previous year.

- An individual with gross profits exceeding Rs. 50 lakhs in any previous assessment year.

- A person who is eligible and registered under presumptive taxation scheme and his/her income exceed the taxable amount.

Section 44BB

The section 44BB applies to Non-Resident Indians (NRIs) involved in the following business of mineral oils industry such as exploration.

Section 44BBB

This section mainly applies to international companies involved in businesses such as civil construction, etc. in specific power projects.

Section 44AD

All the business except those mentioned under Section 44AE, fall under the purview of the Section 44AD.

Section 44ADA

Mainly, this section applies to the regulations related to income tax audits for eligible professionals.

Section 44AE

This section is applicable to the businesses involved in hiring, leasing, and plying of goods carriages.

Apart from these, there are some other tax audits as well. They are as follows:

- Financial Audit

- Construction Audit

- Compliance audit

- Investigative audit

- Information systems audit

- Operational audit

When does the Tax Audit apply?

The audit is applicable in the following cases:

- When the business turnover of the company’s owner surpasses Rs. 1 crore in the financial year.

- When a professional’s gross receipt in profession goes above Rs. 25 lakhs.

How to save yourself from a tax audit?

No doubt, the motive of every business or profession is to derive financial profits. But you should always ensure that your activities aren’t suspicious and illegal, and your records must be clean. Therefore, what you must do to save yourself are:

- As per the Income Tax Act, 1961, you must maintain the accounts book as it is mandatory.

- You must compute the profit or gain as it is computable under Chapter IV.

- You should represent taxable income and allowable loss in tax return file.

- As a taxpayer, you are supposed to file the tax audit report by 30th The earlier you will file, better it would be for you.

Tax Audit Due Date for filing audit report

The due date for filing audit report under Section 44AB of the Income Tax Act, 1961 is 30th September of the assessment year. Therefore, if the taxpayer requires obtaining tax audit, then he/she needs to file an income tax return on or before 30th September with the audit report.

However, if in cases, the taxpayer needs to transfer pricing audit, then the due date for filing the tax audit changes to 30th November of the assessment year.

Penalty for non-compliance

Under any circumstance, if the taxpayer doesn’t get a tax audit done, then a minimum of 0.5% of total sales, gross receipts or turnover or Rs. 1, 50, 000 would be imposed. However, if the taxpayer presents a reasonable cause for the non-compliance, then no penalty would be levied.

Wrapping up

From the above discussion, it’s clear that the tax audit isn’t something that is loved by professionals and business owners. At the same time, it’s not something to be of much worry if you are doing things, carrying your business in the right way and filing returns on time. But you must always ensure that if you fall under the category of taxpayer, then you must file the reports on time to protect yourself from a tax audit.

We hope this blog was helpful for you. If you have any query regarding tax audit, leave a comment below. We will very soon get back to you.

Also, Read:Input Tax Credit under GST