Applicability of GST on Food Industry: A Complete Guide

Shivani Jain | Updated: Jul 30, 2020 | Category: GST, News

In India, the Applicability of GST on Food Industry has always been the topic of Confusion and Dilemma. The reason behind this is that due to continuous change and modification in the tax regime, the Food Businesses are unable to implement all in it.

In this blog, we will talk about the Different GST Rates applicable to the Food Sector in India.

Table of Contents

Applicability of GST on Food Industry

In India, GST on Food Industry depends on several factors and is not restricted to the location and type of establishment. The tax slabs applicable in this sector are 5%, 12%, and 18%.

However, it shall be noteworthy to state that the alcoholic beverages still fall under the ambit of state-level VAT (Value Added Tax). The restaurants, lounges, or any other food outlets engaged in serving alcohol will be charged differently from the outlets or restaurants that deal with food and non-alcoholic beverages.

Further, the GST rates are not only applicable to the items and services offered by the outlets. It is also applicable to the food items and products that an ordinary man purchases. The range of the GST rates pertinent to food items begins from 0% (exempt) to 18% of GST.

Lastly, we know that the VAT and Service Tax regime have already been abolished or repealed after the enforcement of GST. However, the service charge applied by the Restaurants and Food Outlet is different from the GST applied by them.

Overview of the Food Industry in India

As per a report named the ‘Indian Food Services Market Forecast and Opportunities 2020’, published by the TechSci Research[1] , the food service industry in India is expected to rise at a CAGR of over 12% by the end of 2020.

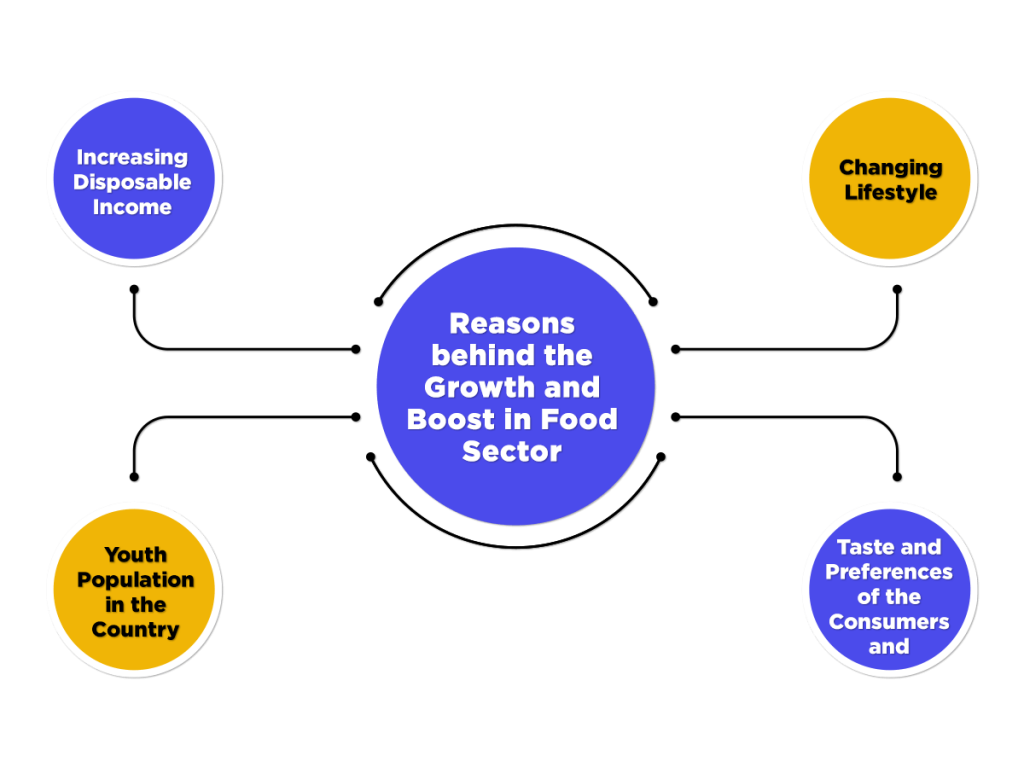

Further, the reasons behind the growth and boost in this sector are as follows:

- Increasing Disposable Income

- Changing Lifestyle

- Taste and Preferences of the Consumers

- Youth Population in the Country

GST Rates on Eating or Food Outlets

| S.no | Description | GST Rates |

| 1. | GST on Outdoor Catering Services | 18% |

| 2. | GST on Food Services, including Food Delivery Services offered by a Restaurant or Food Joint positioned within a premise of a guest house, club, etc. | 18% |

| 3. | GST on restaurant services includes takeaway services and room services provided by the restaurants established inside a hotel offering room tariffs more than Rs. 7500. | 18% |

| 4. | GST on Food Services rendered by both Air Conditioned and Non-Air Conditioned Restaurants and Food Outlets | 5% |

| 5. | GST on Restaurant Services includes takeaway services and room services offered by restaurants located within the building of a hotel charging room tariff below Rs. 7500. | 5% |

| 6. | GST on Meals, food, or food services offered by the government-owned CPSEs, i.e., IRCTC, or Indian Railways, or their licenses in stations, trains, or platforms. | 5% |

| 7. | GST on Non-Alcoholic drinks, beverages, or food served at the mess, cafeteria, or canteen in college, office, school, industrial unit, hostel, etc. on a contractual basis. | 5% |

Note: It shall be relevant to note that GST rates are subject to periodic modifications by government

GST Rates for Food Products

| S.no | Description | GST Rates |

| 1. | GST on chocolate, cocoa, and other chocolate and cocoa products | 18% |

| 2. | GST on food preparations or items that are prepared using flour, malt extract, etc. enfolding cocoa below 40% of the total weight. | 18% |

| 3. | GST on food items such as powder or meal of dried legumes. | 5% |

| 4. | GST on turmeric (fresh turmeric is not included), curry leaves, bay leaves, thyme, rosemary ginger (fresh ginger not included) | 5% |

| 5. | GST on bird’s egg out of egg or shell yolks either boiled by steaming or properly cooked. | 5% |

| 6. | GST on bottle packed meat bearing the registered brand name or trademark | 5% |

| 7. | GST on vegetables that are sun-dried and packed in a container bearing the registered trademark or logo of the brand | 5% |

| 8. | GST on the fresh or chilled meat out of the container | N/A |

| 9. | GST on garden-fresh as well as chilled vegetables, including potatoes, onions, garlic, etc. | N/A |

| 10. | GST on fresh/ cooked/ preserved bird eggs in the shell. | N/A |

| 11. | GST on those vegetables which get preserved and sustained by using different methods that are unfit for direct Human Consumption. | N/A 121 |

| 12. | GST on pasteurised or unpasteurised unsweetened milk, cream, etc | N/A |

| 13. | GST on fresh pears, dried or fresh coconut/ fresh apples, fresh grapes, etc | N/A |

| 14. | GST on boiled/ steamed/ cooked vegetables packed inside a container | N/A |

| 15. | GST on dried leguminous shelled vegetables that are non-container packed despite if skinned/ split or not | N/A |

| 16. | GST on fruits, nuts, vegetables, and various edible parts of the plants that got preserved or prepared by using vinegar or acetic acid | 12% |

| 17. | GST on edible parts of the fruits, plants, nuts, and vegetables preserved or prepared with the help of sugar. | 12% |

Note: It shall be relevant to note that GST rates are subject to periodic modifications by government

Impact of Goods and Service Tax on Food Services

The Impact of Goods and Service Tax on Food Services can be summarised as:

- After the implementation of GST Act, the people who used to have breakfast, lunch, or dinner in the restaurants have noticed an ease in taxation procedure in terms of the bill as GST (Goods and Service Tax) came as a replacement for several taxes and cesses, such as KKC (Krishi Kalyan Cess), VAT (Value Added Tax), and Service Tax. Further, after the applicability of GST on Food Industry, customers have also witnessed the reduction in the tax rates on their restaurant bills. But the reduction in the cost of eating out for customers was noticed to be marginal at best.

- The GST has not impacted the service charge, which is applied by the restaurants on the bill. Therefore, the customers are still paying Service Charge in addition to GST on food.

- Earlier, after the implementation of Goods and Service Tax in India, it was expected that the ITC (Input Tax Credit) would improve the accessibility of the Working Capital Requirement for restaurants. However, in reality, the benefits of ITC available to the owners of the food outlets or restaurant got reduced due to continuous amendments. According to the prevailing GST rules and regulations, only those eateries or restaurants will get to avail of the benefit of ITC who are charging 18% GST. Further, the eateries or restaurants that are charging 5% GST will not be eligible to avail benefit of Input Tax Credit.

- Further, the Goods and service tax exemption have also been provided in the case of fresh and frozen food products or items.

- The Applicability of GST on Food Industry, services, or products will never cross the margin of 18%. That means no food item or product has been classified in the 28% GST Tax Slab, i.e., the highest tax bracket. Therefore, there is no report on the considerable increase or decrease in price after the applicability of GST on food industry and food items.

Conclusion

The applicability of GST on food industry, services, and food items or products has put an end to all the cascading effects of several indirect taxes. In this blog, we have discussed in detail about the GST rates applicable to different food items, together with the applicability of the GST rate on food services.

Moreover, we have also talked about the impact of GST on customers and how they are enjoying the reduction in bill amount after its implementation.

In case of any other confusion and difficulty, reach out to Swarit Advisors, our team of experts will help you in understanding the applicability of GST on Food Industry. Further, we can also assist you with GST Registration, GST Migration, and GST Return Filing, along with FSSAI License and Eating House License, if you want to start a restaurant or eating joint in India.

Also, Read:Online GST Calculator: Easiest Way to Calculate GST Amount